|

|

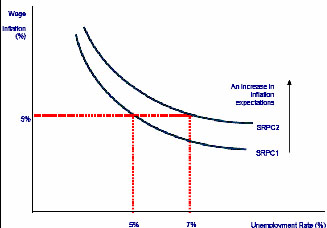

The expectations-augmented Phillips Curve The economist Milton Friedman argued that in the long run, there was no trade-off between unemployment and inflation. He argued that unemployment was not traded with actual inflation but expected inflation. Therefore the Philips Curve was a short run phenomena – changes in levels of unemployment were affected by expectations of rates of inflation. So increasing aggregate demand by monetary expansion increases the expectation that inflation will go up. This shifts the Phillips curve to the right. i.e. unemployment increases because firms expect inflation. Freidman was a monetarist. The monetarist view is that attempts to boost AD artificially to achieve faster growth and lower unemployment have only a temporary effect on unemployment. Friedman argued that a government could not permanently drive unemployment down below the NAIRU – if unemployment is forced below NAIRU higher inflation occurs leading to higher unemployment higher inflationary expectations. This is illustrated in the next diagram – inflation expectations are higher for SPRC2. The result may be that higher unemployment is required to keep inflation at a certain target level. The expectations-augmented Phillips Curve in trying to reduce unemployment below the natural rate of unemployment by boosting AD has little success in the long run. What happens instead is to create higher inflation with increased inflationary expectations. Monetarists believe inflation is best controlled through tight control of money and credit. Credible policies to keep on top of inflation can also have the beneficial effect of reducing inflation expectations – causing a downward shift in the Phillips Curve. Long run Phillips Curve This is drawn as a vertical line i.e. the long run Phillips curve is no more than NAIRU (non accelerating inflation rate of unemployment) Reducing the long run Phillips Curve (or NAIRU), i.e. shifting the LRPC to the left, can be brought about by supply-side policies example labour market reforms might be successful in reducing frictional and structural unemployment – perhaps because of improved incentives to find work or gains in the human capital of the workforce that improves the occupational mobility of labour. |